WELCOME TO VIKING-INVEST

Risk management with real options - Real options the easy way

BERGEN NORWAY

REAL OPTIONS IN SHIPPING

Real options analysis (ROA) is the futures method for solving investment decisions dealing with real investments where uncertainty is a dominant element such as in shipping. Real options (RO) are characterized by a dynamic decision process, which includes operating (managerial) flexibility. The advantage of using RO is therefore clear; the operator can assess the value of flexibility and develop an investment strategy. ROA can evaluate the value of taking corrective action when the freight rate changes, the operator can postpone operations, expand the fleet, scale down the fleet or abandon a project when new information about the rate is available. This makes the project more robust and is a form of risk management where the operator can limit downside risk and increase upside potential. To put it another way the operator can adapt to a new reality or event when new information about the rate is available, and can take corrective action such as a Plan B, Plan C or Plan D.

A DECISION MODEL FOR REAL OPTIONS ANALYSIS IN SHIPPING

Viking-Invest uses in most cases decision tree analysis (DTA) and this is implemented in a spreadsheet such as Excel at a low cost. In some cases we use DTA in combination with heuristic optimization and this is a more advanced model. Heuristic optimization is method where you search and find a solution and you are not guaranteed to find an optimal solution, but it’s sufficient to meet the objectives. The model helps the operator to choose the investment strategy for the fleet that is in line with the operator’s risk-return profile. And since there is usually three scenarios for the rate after optimization this gives a clear risk-profile with “best”,” expected” and “worst –case” scenarios, where every scenario has a clear defined discrete probability. Traditional static expected net present value analysis does not capture the element of flexibility and is not dynamic, and therefore can’t be used to evaluate an investment strategy for the fleet.

The figure under is a decision tree and the simplest real option model. This is a two-phase investment analysis model where we have one investment decision “here and now” in phase 1.In phase 2 we have the following 3 corrections: “charter in an additional ship”, “Time charter 5 years and thereafter on the spot market” and “lay-up 5 years and thereafter on the spot market”. The optimal decisions and our strategy are represented in the grey shaded boxes. Our models are usually much larger with up to 9 corrections in each freight rate scenario. And the larger models are difficult to present as a decision tree because of the size.

Fig. 1 A SIMPLIFIED EXAMPLE: A simple two-phase investment analysis model and that is represented as a decision tree

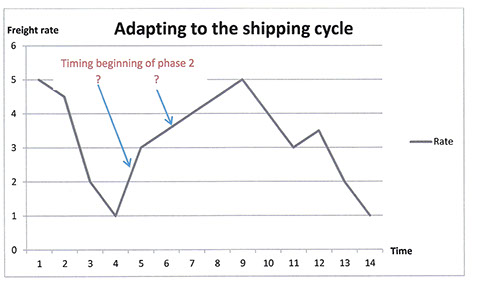

ADAPTING TO THE SHIPPING CYCLE

Shipping is an extremely cyclic business where the freight rate changes substantially both on the short and long term depending on the trade and market segment. Our models capture the element of timing the correction to the optimal stage in the cycle. In example we can choose when to exit or enter lay-up, when to invest or sell (asset play) and when to changes all kinds of chartering policies. This means we determine when phase 2 and the correction starts with plan B, plan C etc. like the examples mentioned above.

Fig. 2 Determine when phase 2 begins and the corrections start in the shipping cycle. In example we determine when to enter or exit lay-up, when to correct the chartering policy, when to buy or sell a ship etc.

Fig. 3 Determine when corrections and phase 2 begin. Adapting to the shipping cycle. There is a connection between decision in phase 1 and corrections in phase 2, where the first decision determines possible corrections in phase 2.

Fig. 4 A SIMPLIFIED EXAMPLE: Heuristic model with timing and here the model is visualized by a simple decision tree. Determining when phase 2 and corrections begin.

SUMMING UP THE REAL OPTION MODELS

- One factor models where the freight rate is a stochastic variable with 9 states and all other uncertain variables such as ship prices, scrap prices etc. are derived from the rate.

- Our models are dynamic models and are referred to as a “two-phase investment analysis model” and can evaluate operating flexibility or real option analysis.

- A spin-off from the models is that if they are modified they can be used to calculating forward freight agreement (FFA).

- Trinomial models with 3 scenarios after optimization: “Best”, “Expected” and “Worst” scenarios.

- Heuristic model: Not guaranteed to find optimum and the operator by testing and failing searches for a solution that is sufficient to meet the objectives. The models are designed such that the optimization procedure goes efficient and speedily.

Typically up to 9 real options or corrections in all real option models

All options mentioned under are stochastic and derived from the freight rate with 9 states except the option “lay-up” which is deterministic.

- 3 options to expand: “Buy second hand ship”, “Build ship” and “charter in ship”

- 2 options to contract: “Charter out” and “Lay-up”

- 2 options to abandon: ”Sell a ship” and “Scrap a ship”

- 2 options for chartering policy: “Spot market” and “Time charter”

Basically 2 different real option models

- One model where the rate is treated exogenously and suitable for treating different types of flexibility. Here we can include market sentiment and psychology in the market when calculating the freight rate which is stochastic.

- One holistic physical market model where the rate is an endogenous variable and is derived from the physical market with supply and demand. We calculate here a piecewise supply function (see Fig. 5). The supply from a ship owner is a form of "strategic variable" and with the total market supply determines the rate. Here there is no market sentiment or psychology in the model. Suitable for all types of flexibility. Forecasting is integrated in the model and thereby a holistic model. Because of the special J shaped supply function we have most of the time excess supply and low freight rates and in rare occasions very high rates with super profit earnings. This characteristic supply function should therefore be included in the real option analysis

Fig. 5 EXAMPLE: The supply function in the physical market model